March 25, 2022

Overview of the new SEC proposed mandate on climate risk disclosure

Click here to download a PDF version of this article.

On March 21, 2022, the U.S. Securities and Exchange Commission (SEC) proposed long anticipated rule amendments that would require publicly traded companies to include climate-related disclosures in public filings, such as on Form 10-K, offering a detailed picture of a company’s governance, risk management, and strategy with respect to climate-related risks. The proposed climate disclosure rules are now open for a 60-day public comment period and will likely be finalized by the end of 2022.

The proposed rules come in response to investors and other stakeholders who have become increasingly concerned about the risks associated with climate change on financial markets and companies’ bottom lines. This shift is highlighted in the 2022 Letter to CEOs from BlackRock CEO Larry Fink, who noted that setting and meeting greenhouse gas (GHG) reduction targets is critical to the long-term economic interests of companies.

Pressure has been building for more consistent, comparable, and reliable reporting of potential climate impacts to businesses, aligned with existing financial reporting. The new requirements aim to increase consistency and reliability in reporting, and provide companies and investors with “clear rules of the road” to better manage risk, as noted by SEC Chair Gary Gensler in his Statement on Proposed Mandatory Climate Risk in Disclosures. According to the SEC, its decision was guided by the concept of “materiality,” as clarified by the Supreme Court (Basic Inc. v. Levinson,1988) — that information is material if there is significant likelihood that a reasonable shareholder would consider it important in making an investment or voting decision.

What’s included in the climate disclosure rules?

The proposed rules would require companies to disclose their GHG emissions along with detailed disclosures on climate-related financial risks, similar to those in widely accepted accounting and disclosure frameworks, such as the Greenhouse Gas Protocol (GHG Protocol) and the Task Force on Climate-Related Financial Disclosures (TCFD), respectively. This includes disclosure of any relevant risk management plans and transition plans in place, information on climate-related targets and goals, renewable energy certificate (RECs) and offset procurements, and any internal carbon prices. All disclosures would be phased in between 2023 and 2026, depending on registrant type.

Companies would be required to report on their Scope 1 (direct emissions) and Scope 2 (indirect emissions from purchased electricity) emissions, which become subject to assurance (i.e., third-party expert review) as early as fiscal year 2024. Companies will also be required to report Scope 3 emissions (emissions from upstream and downstream activities in their value chain) if material or if included in any emissions targets. For purposes of the rule, Scope 3 emissions would be considered material if there is a substantial likelihood that a reasonable investor would consider it important when determining whether to buy or sell securities or how to vote.

Beyond emissions, companies will need to disclose their processes for identifying, assessing, and managing climate-related risks, and the anticipated financial impacts associated with climate-related physical (e.g., extreme weather events) and transition risks (e.g., carbon prices) likely to affect their strategies, business models, and outlooks. Companies will also need to disclose information about the oversight and governance of climate-related risks by their board and management.

Scope 3

As noted in the proposed rules, commentors expressed concern during rule development over the availability and quality of data coming from suppliers and other third parties necessary in calculating Scope 3 emissions. For many organizations, a majority of emissions are embedded within their supply chains and the products and services they sell, meaning that the inclusion of Scope 3 GHG emissions is an important input to ensuring that investors are aware of a company’s full exposure to climate-related risks. However, quality and consistent data can be a challenge to obtain.

To account for potential difficulties associated with calculating Scope 3 emissions versus Scope 1 and 2, a safe harbor accommodation is included for Scope 3 emissions disclosure, as long as emissions are reported with a reasonable basis and in good faith, and a reporting exemption is provided for smaller reporting companies (SRC).

What does this mean for your organization?

To begin preparing for the proposed rules, companies can develop the governance frameworks to establish a comprehensive understanding of existing climate initiatives and identify potential gaps to meet SEC proposed requirements. Depending on the gaps identified, this may necessitate establishing processes to reliably calculate and report on GHG emissions and climate risks and opportunities. Voluntary reporting following the GHG Protocol, including all Scope 3 emissions, will establish a reliable data pipeline to support future reporting, including sources that may be considered material.

Companies that begin exploring opportunities to abate their emissions and evaluate GHG reduction goals in alignment with leading frameworks (e.g., standards set forth by the Science Based Targets Initiative (SBTi)) will be well-positioned to begin managing climate risk by preparing to operate in a low-carbon economy. Companies can also begin building internal capacity and insight into climate exposure by voluntarily evaluating climate-related risks and opportunities, and their potential financial impacts, through TCFD disclosure and scenario analysis.

What’s next?

The SEC’s proposed climate disclosure rules are now open for a 60-day public comment period and will likely be finalized by the end of 2022. Written comments during this period can be submitted to the SEC online, via e-email, or by mail, following instructions posted on the SEC’s webpage.

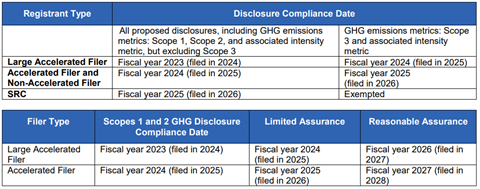

The SEC has proposed a preliminary timeline for when these disclosures will be phased in for companies of varying sizes and their respective reporting obligations, with Scope 3 disclosures being phased in after Scopes 1 and 2.

Source: SEC Enhancement and Standardization of Climate-Related Disclosures Fact Sheet

How can Edison Energy help?

Edison Energy is here to help. We work with our clients to establish robust climate governance, decarbonization strategies, and implementation frameworks, partnering with companies at all levels of sustainability maturity. We work with clients to measure Scope 1, 2, and 3 GHG emissions; set climate-related targets and goals (e.g., science-based targets (SBTs) and Net-Zero goals); devise and implement decarbonization strategies and transition plans, including energy optimization and renewable energy initiatives; and identify, evaluate, and disclose climate-related risks and opportunities in alignment with TCFD recommendations. Edison can help support companies looking to understand their obligations under these proposed rules and how to prepare for and go beyond the mandated disclosures.

Contact us

Tim Kidman

Managing Director, Sustainability Strategy

tim.kidman@edisonenergy.com

Annabelle Stamm

Director, Sustainability Strategy

annabelle.stamm@edisonenergy.com